Homeowners insurance is very important. It protects your home, what’s inside, and your other assets in the event of disasters, accidents, theft and more. Insurance varies from standard coverage to additional coverage that includes floods, earthquakes, etc. However, not everyone wants the same coverage for their home, apartment or condo.

Everyone has different needs and talking about the precautions and evaluations of those needs can help protect your family and make the most of your insurance coverage. Meet with your insurance agent every year to review your policy. They can help you find the best policy and coverage for your particular needs.

Here are some questions to keep in mind when looking for the right coverage for you:

Has your home recently suffered damage due to storms, accidents or anything of the sort?

Has your home been remodeled or expanded?

Do you have money set aside to cover the deductible if you have a loss? (For most homes in Florida, the insurance deductible is 2 percent of the policy limits.)

Do you have an inventory of your possessions?

Do you have flood insurance?

It’s also important to know what windstorm mitigation features the home has. This will impact the Florida Homeowners policy that you will buy and how much will it costs.

Features such as hurricane shutters, new roof will impact the type of policy you should have.

At L and C insurance providers we provide 10 different Homeowners insurance policies that can help provide the best coverage at the best possible rate.

The perfect storm that has been brewing in Florida’s property insurance marketplace has finally made landfall—and it’s wreaking havoc on homeowners insurance rates.

The three leading causes of premium spikes include Assignment of Benefits fraud, Hurricane Irma, and reinsurance claims. Let’s look at the impact of these three factors to answer the question: why is Florida homeowners insurance going up?

Cause No. 1: Assignment of Benefits Fraud

What is an AOB?

An Assignment of Benefits (AOB) is an agreement that transfers a homeowner’s insurance claims rights to a third party. Signing an AOB form gives someone else the power to file claims, make repair decisions, and collect insurance payments on the homeowner’s behalf.

For example, if a home is damaged, a homeowner calls a repair contractor, like a roofer or plumber. The contractor then gets the homeowner to sign an AOB. That contractor is now free to file a claim on the homeowner’s behalf and directly collect a check from the insurance company.

Entering into an AOB agreement seems like a tempting offer since most homeowners prefer not to be involved in the claims process. However, handing over insurance claims rights to a contractor is hardly ever a good idea.

How AOB Scams Work

Many things can go wrong when a contractor works directly with an insurance company. Without the homeowner’s oversight, they can easily overestimate the value of their work to pocket more money. When an insurance company recognizes an amount has been inflated and refuses to pay the padded bill, the contractor may hire a lawyer and sue the insurance company. And without realizing it, the homeowner becomes embroiled in a messy, pricy lawsuit.

How does AOB fraud impact homeowners insurance ?

Both insurance companies and homeowners pay a steep price for AOB abuse. Insurance companies are forced to either pay inflated repair bills or sue contractors and pay for the cost of defense, whether they fight, or settle, that lawsuit. As a result, many carriers must petition for higher rates or stop issuing policies in Florida. Homeowners, on the other hand, get stuck with costly and substandard repairs, hefty lawyer’s fees, and, consequently, higher insurance premiums.

Every Florida homeowner with an insurance policy—even those who play by the rules—ends up paying the price for AOB abuse. That’s why it is crucial homeowners be able to spot home repair insurance scams.

Cause No.2: Hurricane Irma

The storm’s statewide devastation

Hurricane Irma struck Florida twice on September 10, 2017, first as a Category 4 at Cudjoe Key and then again as a Category 3 on Marco Island. The storm unleashed 130 mph winds, spawned 23 tornadoes, and produced heavy rain across the state. By the time Irma crossed the border into Georgia as a tropical storm on September 11, it had caused close to $50 billion in damages, making it the costliest hurricane in Florida’s history.

Irma’s impact on the insurance market

While Hurricane Irma hit Florida in 2017, insurance companies saw claims from the storm steadily increase through 2019—two years after the storm’s initial impact. That’s because a statewide law gives Florida homeowners up to three years from the date a hurricane makes landfall to report a hurricane claim.

Irma’s cost to homeowners today

The high number of re-opened claims over three years, combined with AOBs, led to claims inflation and steady loss creep, which factored into this year’s reinsurance renewals. As a result, Florida homeowners faced significant insurance rate hikes in 2020.

According to Reinsurance News’ directory of major insurance and reinsurance loss events, Hurricane Irma resulted in an overall economic loss of $67 billion, including a reinsurance industry loss of $32 billion. But what is reinsurance, and how does it factor into homeowners insurance cost?

Cause No. 3: Reinsurance Claims

What is reinsurance?

Dubbed “insurance for insurance companies” by the Reinsurance Association of America, reinsurance is a form of insurance purchased by carriers to lower their risk.

The goal is to make sure no single insurance company is exposed to a significantly massive disaster—like a hurricane.

Because in the insurance business, it’s a matter of when (not if) disaster strikes. Reinsurance limits the amount of loss an insurance company can potentially suffer, which protects them from financial ruin and policyholders from uncovered losses.

Why reinsurance matters to policyholders

Reinsurance protects carriers from bearing the entire financial toll of a catastrophic event, like Hurricane Irma. And by transferring portions of their risks, insurance companies can make their premiums more affordable for homeowners. That’s a good thing for policyholders.

How reinsurance factors into homeowners insurance costs

Between 2005 and 2016, not a single hurricane made landfall in Florida. But the tides changed after a slew of hurricanes, including Harvey, Irma and Maria, made landfall in 2017, costing close to $283 billion in damages and resulting in one of the costliest loss years on record for the insurance industry. Meanwhile, the estimated insured losses for 2018’s Hurricane Michael in Florida reached $7.4 billion, according to the Florida Office of Insurance Regulation.

For insurance carriers, the increase in the intensity and frequency of extreme weather events, such as major hurricanes, has drastically changed the cost of doing business in Florida. When factored into reinsurance renewals, the costs of the 2017-2018 hurricane season alone caused significant rate hikes for Florida homeowners in 2019 and 2020.

What’s on the Horizon

AOB fraud, Hurricane Irma, and reinsurance costs have all contributed to rising homeowner insurance rates for Floridians. However, there has been some reform, especially regarding AOB scams.

In May 2019, Florida Governor Ron DeSantis signed House Bill 7065: Insurance Assignment Agreements, which addressed AOB abuse. The reform bill aimed to curb AOB fraud which has resulted in rising insurance costs for Floridians. (Download our quick guide on how to avoid falling victim to AOB fraud and abuse).

“I thank the Florida Legislature for passing meaningful AOB reform, which has become a racket in recent years,” DeSantis said. “This legislation will protect Florida consumers from predatory insurance practices.”

While reforms for Florida’s AOB crisis helps address some of the costs, there will always be hurricane-related losses, especially since homeowners have three years from the date a hurricane makes landfall to file for loss or damages. And that means demands for rate increases from reinsurers aren’t likely to drop anytime soon, forcing insurance companies to increase premiums for homeowners.

Water damage is one of the leading claims filed by homeowners and accounts for billions of dollars in losses annually in the U.S. Yet many homeowners are unaware of what types of water perils are—and are not—covered by their home insurance policy. Unfortunately, this can put homeowners in a slippery and stressful situation. Imagine having to file a water-related claim, and then discovering the damage is only partially covered—or worse, not covered at all by your home insurance policy. Does your homeowners insurance cover water damage and common water perils? Let’s find out…

Does Home Insurance Cover Broken or Burst Pipes?

Whether caused by clogs, water pressure spikes, or even frozen water, burst pipes are one of the top causes of water damage in homes. Excessive water force may cause pipes to swell and eventually break, spouting water everywhere and damaging floors, carpeting, drywall, and insulation.

Facts about Leaky and Burst Pipes

The average home loses 14 percent of its water to leaks.

Water-damage claims, mostly from leaky or burst pipes, are the leading cause of increased home insurance rates.

Water damage caused by plumbing failures and frozen pipes is the second leading cause of property loss.

What Type of Insurance Do I Need?

Water damage from a burst pipe is typically covered under a standard HO3 homeowner’s insurance policy. However, damage caused by sewer and drain backups is not usually covered. For complete protection in case of a backup-related incident, you can add sewer backup coverage to your policy.

What’s Covered?

Most HO3 homeowners policies cover water damage caused by a burst pipe as long as the incident is sudden and accidental. If water damage occurs outside of your home, you’ll need to be able to demonstrate that a burst pipe was the culprit. Keep in mind that water damage resulting from unresolved maintenance issues, such as ongoing leaking near a sink faucet or washing machine, will probably not be covered, and your claim may be denied.

Does Home Insurance Cover Floods?

A flood is any overflow of water caused by storm surge or rising water from heavy rain—something you see a lot of in Florida. Remember, you don’t need to live near a lake, river or the coast to experience a flood.

Facts about Floods:

Floods are the leading natural disaster in the U.S.

25 percent of flood losses come from low- to moderate-risk areas in Florida.

On average, as little as two inches of water in your home can cause $7,800 or more in damage.

What Type of Insurance Do I Need?

Losses due to flooding are not typically covered under your home insurance policy, so we recommend purchasing a supplementary Florida Flood Insurance policy for complete protection. Flood insurance policies are issued by First Community Insurance Company, which is authorized by the Federal Emergency Management Agency (FEMA) to sell flood insurance. In some flood zones, you can purchase flood insurance for about $1.40 per day, and it’s 100 percent guaranteed by the U.S. government. Remember, flood insurance requires a 30-day waiting period before it’s activated, so don’t delay.

What’s Covered?

Flood insurance covers damage caused by overflow of inland or tidal waters that have inundated two or more properties, at least one of which is yours. Keep in mind that flood damage from wind-driven rain is not covered under flood insurance. When rain enters your home through a wind-damaged window, door, wall, or roof, the National Flood Insurance Program considers the resulting damage to be windstorm-related, not flood-related.

Does Home Insurance Cover Wind-Driven Rain?

Windstorms are weather events that produce winds and violent gusts strong enough to cause significant property damage, such as hurricanes and tornadoes.

Facts about Windstorms:

Windstorms can have wind speeds exceeding 200 miles per hour.

Heavy winds cause about $1 billion in damages in the U.S. every year.

Approximately 85 percent of all windstorm-related insurance claims result from roof damage.

What Type of Insurance Do I Need?

Windstorm insurance covers damages caused by hurricane-force winds, tornados, hail, and other weather events with wind gusts exceeding 35 miles per hour. In hurricane-prone states like Florida, you may be required to purchase a separate windstorm policy to provide complete protection of your home.

What’s Covered?

Windstorm insurance typically covers damages to the structure of your home and the personal belongings inside of it. Most policies also include coverage for detached structures such as garages, sheds, and swimming pools. Windstorm events like hurricanes are often followed by storm surge and flooding, which are not covered. A flood insurance policy must be purchased separately to cover any damages related to flooding, even if the flooding was caused by a windstorm.

Does Home Insurance Cover Mold?

One common and gross side effect of water damage is mold. In addition to being hazardous to your health, mold can depreciate the value of your home by discoloring walls and ceilings, rotting wooden floorboards and siding, destroying insulation, or emitting a musty odor.

Facts about Mold:

The most common indoor molds are Cladosporium, Penicillium, Alternaria, and Aspergillus.

Mold can cause nose stuffiness, coughing or wheezing, and irritation of the throat, eyes and skin.

What Type of Insurance Do I Need?

Most home insurance companies cover mold growth resulting from a covered water peril. While some companies have begun taking steps to avoid or limit their exposure to mold claims , People’s Trust understands that mold must be promptly remediated in order to prevent further damage.

What’s Covered?

Your standard HO3 homeowner’s insurance policy will most likely cover the costs of eliminating mold caused by a burst pipe or other covered water peril. However, your policy will not cover the cost to remove mold caused by neglected maintenance issues, such as ongoing water leaks, humidity problems, or landscaping and drainage issues. Additionally, mold that develops from flooding will not be covered under your standard homeowner’s policy.

Does Home Insurance Cover Roof Leaks?

There’s nothing more comforting than knowing you have a safe roof over your head. Your home’s roof is the first line of defense in protecting you and your belongings from earth, wind, and fire (and more)! But even roofs have their weaknesses…

Facts about Roof Leaks:

Roofs, on average, last only half of their designed lifetime.

Moisture from leaking roofs causes more damage to homes than termites, fires, and storms combined.

40 percent of all building-related problems are caused by water entering through the roof.

What Type of Insurance Do I Need?

A standard HO3 homeowner’s insurance policy typically covers water damage caused by a roof leak. Whether or not it’s covered depends on the cause of the leak.

What’s Covered?

If the roof leak was caused by Mother Nature (e.g. rain, hurricanes or tornadoes) or other sudden, uncontrollable events, your home insurance policy will likely cover the cost of the associated water damage. On the other hand, roof leaks resulting from failure to maintain your roof as it ages will not be covered. That’s why it’s so important to have your roof inspected and repair or replace it as needed. Because carrier rules and regulations differ among home insurance companies, it’s important to review your policy to make sure you have the insurance you need so you can enjoy peace of mind knowing your home is covered in the event of a water loss.

Many people consider buying a second home for several reasons, including:

Vacation home

Rental property

Tax benefits

Long-term profits

Flexibility in where you live

No matter what reason you choose to buy a second home, it’s important to protect your large investments with insurance. Just like your primary home, you should obtain homeowners insurance with coverage appropriate to the location of your second dwelling. However, it is essential to understand that there are special considerations for your second home that you may not be aware of.

Check Your Primary Homeowners Insurance Policy

First, check your current homeowners insurance policy to see if it will cover a second home. Some policies may extend coverage, which could make insuring your second place a breeze. However, many insurance companies only cover one home because every home is unique and comes with its own coverage needs. For instance, your vacation home may be in a high-risk area for floods or earthquakes.

Another example could be that your new property is in an area that is prone to vandalism or theft. No matter the reason, it’s important to consult with a homeowners insurance company in your area to assess the needs of your second home.

Insurance Considerations for Your Second Home

Buying an insurance policy for your second home is a lot like buying a policy for your primary home. However, there are some risk factors associated with second homes that may change your insurance rate. Before purchasing a new insurance policy, you should determine the coverage needs for your second home. Many factors will play a significant role in the home’s coverage, including:

How often the home is lived in

The location of the second home

The features included with the second home

Any natural hazards near the second home (such as a 100-year floodplain)

How Often the Home Is Occupied

Second homes may not be used or occupied as often as primary homes, especially if it’s a vacation home. The home vacancy is considered a risk for insurance companies, which can increase your rates. There are a few reasons that home vacancy is considered a higher risk:

The home could be more prone to theft and vandalism

Second homes could have more hazards that go unnoticed

Accidents could occur that you would be liable for even if you weren’t there

For instance, if someone uses your pool and has an accident, you could be held liable for their medical bills and legal expenses, even though you weren’t at your home.

Location

Homeowners insurance can vary by location. Insurance companies look at the region you live in, the type of neighborhood, and even the street you live on to determine how much you should pay in premiums. Factors that increase home insurance rates include:

Whether your primary insurance company provides coverage in that area

The local crime rate

The home value

The replacement costs

While it’s always a good idea to check with your primary insurance company first, it may not provide coverage outside the region where your first home is. Having to go with a different company may eliminate the possibility of bundling policies or enjoying other discounts.

Many people use their second homes as vacation homes, which are often located in unique places like mountains or beaches. These environments may need specific coverage to protect against natural disasters like floods, hurricanes, and earthquakes.

Home Amenities

Some amenities can increase your insurance rates due to liability risks. If you are looking to outfit your second home with luxuries, there are a few things to consider:

Pools and hot tubs: These amenities can increase the replacement value of your home as well as increase your liability risk. The increased risk of accidents, like drowning, for example, can increase your premium.

Finished basements: Damage to a finished basement from flooding or burst pipes is more likely to result in a claim than an unfinished basement. These claims could raise your insurance premiums down the line.

Expensive items: Homeowners insurance can cover luxury items inside the home but only up to a certain amount. You may need to obtain additional insurance if you would like your possessions protected.

Wood-burning stove or fireplace: This amenity is more at risk of fires and smoke damage than gas stoves and fireplaces.

Natural Hazard Risk

Depending on where your second home is located, you may be at higher risk for sustaining damage due to a natural disaster. Typically, major disasters like earthquakes and floods are not covered under a standard homeowners policy, and you would have to purchase additional coverage to protect your second home. Depending on the area, you may need to inquire about add-ons to protect against:

Flood: This is usually indicated if your property sits within a 100-year flood zone and if it is near a major body of water like a lake or the ocean.

Hurricane: Hurricane paths can be unpredictable, but generally, your state or local government will either strongly encourage or require coverage for hurricanes if you are in a high-risk area.

Ground Movement: Most people are familiar with earthquakes, but this type of coverage also protects against damage due to sinkholes. Both types of disasters can be devastating to homeowners, and neither is typically included in standard policies. You’ll want to investigate the area where your second home is located to learn about any fault lines or risk factors that may indicate sinkholes to determine if this coverage is necessary.

Hail: This is less a regional risk and has more to do with the age and condition of your roof. Hail damage can occur virtually anywhere, and roofs more than 10 years old may be more expensive to insure—or simply won’t be included in a basic policy.

Ultimately, the coverage add-ons you need will depend heavily on where you opt to purchase a second home, and the research you do into local risk factors and weather trends.

Purchase a Second Home Insurance Policy

Since second homes are typically deemed riskier than primary homes, the home insurance premium tends to be more expensive. Consider bundling your home insurance policy with another kind of insurance coverage to keep premiums as low as possible. Some companies will discount your insurance premiums if you choose to bundle. The most common bundling scenario is home and auto insurance; however, depending on your provider, you may be able to bundle more.

Another option is to upgrade the security at the second home. This upgrade can help lower the risk of loss from burglary and accidents. Additionally, some insurance companies may give discounts to customers who install smart home security features since home security typically falls under protective device discounts.

Protect Your Second Home

To further protect your second home, there are additional steps you can take, including:

Obtaining additional coverage, including contents coverage which further protects your possessions in your home

Asking friends and neighbors to keep an eye on the house

Hiring a seasonal caretaker

Putting lamps on timers to turn on and off, creating the illusion that someone is home

Installing risk-prevention systems, like water leak sensors

Buying a home that is part of a homeowner’s association

A second home may be part of your financial goals. However, there is a lot to consider when it comes to protecting your investment. By understanding the insurance considerations and knowing how much coverage is needed, you can make more informed decisions on your insurance policy for your second home.

Shopping for a new home is an exciting time for many Floridians, but few know that the home they choose could make or break their home insurance rates.

Whether you’re searching for an already built home or planning to construct one from the ground up, there are some important factors to consider before you purchase your dream home.

Is Hazard Insurance the Same as Homeowners Insurance?

If you are applying for a mortgage or shopping around for homeowners insurance, you may encounter a variety of terms defining the types of insurance you can purchase and what is included in your policy. Hazard insurance is not a separate policy from homeowners insurance. Instead, it is a specific coverage included in most homeowner’s insurance policies.

Hazard insurance provides specific coverage related to the structure of the dwelling. Besides covering hazard insurance, most home insurance policies will provide additional coverage for other types of damages, such as casualty insurance and liability coverage if someone sustains an injury on the property. Typically, homeowners insurance will contain the following coverages:

Hazard coverage

Dwelling coverage

Additional structure coverage

Personal property coverage

Loss of use coverage

Personal liability coverage

Medical payments coverage

What Is Hazard Insurance?

Hazard insurance provides coverage specific to the structure of your home. When asking about the types of insurance you need, lenders will often specifically ask for a hazard insurance policy to ensure that if they issue you a loan at minimum, the structure on the property is covered. Because lenders often ask for hazard insurance specifically, the term’s everyday use has become ambiguous with its true definition.

What Does Hazard Insurance Cover?

Hazard Insurance typically provides coverage in two distinct types; named perils and open perils. Named perils will be specific to your policy and ensure coverage. In contrast, open perils are perils covered that are not explicitly named in your policy. Named perils may include:

Home fires and fires caused by natural disasters

Smoke damage

Theft

Vandalism

Explosions

Wind and damage caused by wind storms, such as falling trees

Hail

Lightning and burn damage caused by lightning

Damage from vehicles

Damage from aircraft

Damage from riots or civil commotions

Damage from volcanic eruptions

Falling objects

Damage from freezing pipes or AC

Accidental damage from electrical currents

Damage from the weight of snow, ice, or sleet

Open perils typically cover everything except the following:

Earth movements, such as damage from earthquakes

Ordinance of law and government action

Some types of water damage

Damages from power failures

Damages from neglect of the property

War

Theft during active construction

Intentional loss

Mold, fungus, or wet rot

Smog, rust, and corrosion

Discharge and seepage of pollutants

Birds, vermin, rodents, and insects

Damage to the property from animals that you own

Normal wear and tear of the dwelling

It is vital to review your insurance policies to understand what your personal policy lists and provides coverage for. Every policy may be unique and may not cover the same types of damage as previous policies you may have had.

Hazard Insurance Claim Reimbursement

If damage occurs to the dwelling covered by hazard insurance, you will be required to first pay the amount defined by your deductible, and the insurer will cover the remaining amount. Your reimbursement will depend on the reimbursement provisions in your policy, typically boiling down to one of the two following:

Actual cash value. Actual cash value is typically the least expensive policy to purchase and often offers the smallest amount of reimbursement for damages. Actual cash value provides reimbursement for what your property was worth—including any wear or tear and depreciation at the time it was damaged or destroyed.

Replacement cost value. Replacement cost value typically comes at a higher expense but provides reimbursement for the property—regardless of depreciated value. This means that your coverage replaces the damaged or stolen property at its full cost for a brand new item—regardless of wear, tear, and depreciation.

Is Hazard Insurance Required?

Homeowners’ policies and those that include hazard insurance are generally not a legal requirement. However, if you are applying for a mortgage or purchasing your home through a loan, your lender may require you to have a homeowners insurance policy that includes hazard insurance. This lender requirement ensures the lender that if something happens to the dwelling on the property, the asset is covered and financially protected. Some lenders may require you to pay a year’s worth of premiums on the insurance policy in advance of signing a home loan.

While obtaining homeowners insurance and subsequently hazard insurance may not be a legal requirement, it is best to get as much coverage as you can to ensure that your property and valuables are protected in the event of theft, vandalism, accidental damage, or damage caused by unforeseen events such as the weather.

If you own a property that you wish to use as a second home, you may need to consider homeowners insurance for second homes and vacation properties that include hazard insurance or a landlord insurance policy. Choosing between these types of policies will depend on your personal situation and individual needs.

How Much Is Hazard Insurance?

The cost of a homeowners insurance policy that includes hazard insurance will depend upon a few factors that include:

The value of the property and dwelling

What is included in the policy

The policy limit

The deductible amount

If you choose reimbursement as actual cash value or replacement cost value

Considerations for selecting your insurance will depend on your personal budget and how much you can afford, as well as the type of coverage you decide is necessary to keep your property, dwelling, and personal belongings covered for reimbursement.

For example, you may choose to pay a smaller premium for an insurance policy that does not provide extensive coverage and only offers actual cash value. In the event of damage, your property may not be covered, or you may end up paying more to replace your damaged items.

If you choose a policy with more extensive coverage that includes replacement costs, you may rest assured knowing that your assets are protected; and that you will receive full reimbursement to replace your damaged items or property

Shopping for a new home is an exciting time for many Floridians, but few know that the home they choose could make or break their home insurance rates.

Whether you’re searching for an already built home or planning to construct one from the ground up, there are some important factors to consider before you purchase your dream home.

How Old Is It?

An older home may be charming and filled with snippets of Florida’s history, but it can also cost more to insure. This is because older homes tend to develop problems more often than newer ones. If you choose to purchase an older home, you can help reduce your home insurance rate by making renovations designed to prevent common problems associated with electrical wiring, plumbing, roofing, and foundation. Before starting any renovations, consult with your home insurer to make certain.

Additionally, many Florida home insurance companies offer discounts for purchasing a new home because new structures are generally built with the latest safety codes. In 2001, the state implemented the Florida Building Code, which was designed to protect lives, help reduce property losses in a major storm, and provide a guide for home insurance companies to determine rates.

Improvements under the Florida Building Code include:

• Better structural design requirements to withstand greater wind pressures in South Florida and most coastal areas • Wind-borne debris protection required on windows in all coastal areas and South Florida • Improved roof covering systems requirements • Approval system that ensures that products comply with wind resistance and impact resistance requirements • Improved window performance labeling requirements

A 2005 study conducted by the University of Florida revealed that homes built in 2002 or later sustained less damage from hurricanes than homes built between 1994 and 2001 under the Standard Building Code. Homes constructed prior to 1994 fared even worse.

The study found that shingle-roofed homes built under the Florida Building code experienced less shingle damage than homes built under the 1994 code. This is critical in hurricanes because loss of too many shingles can compromise the roof and allow rain to enter the home.

The study also discovered that none of the homes built after the requirement for reinforced garage doors sustained significant garage door damage. Meanwhile, garage doors on most homes built prior to 1994 were blown off their tracks, which allowed wind to enter the house and undermine the integrity of the roof from inside.

What Building Materials Were Used?

The materials used to build your home can also influence your home insurance rate. For example, it’s more expensive to insure a wood frame home than one constructed out of brick. Homes made out of wood materials are more prone to fire and wind damage, making them a greater risk than brick homes that are built to withstand these types of hazards.

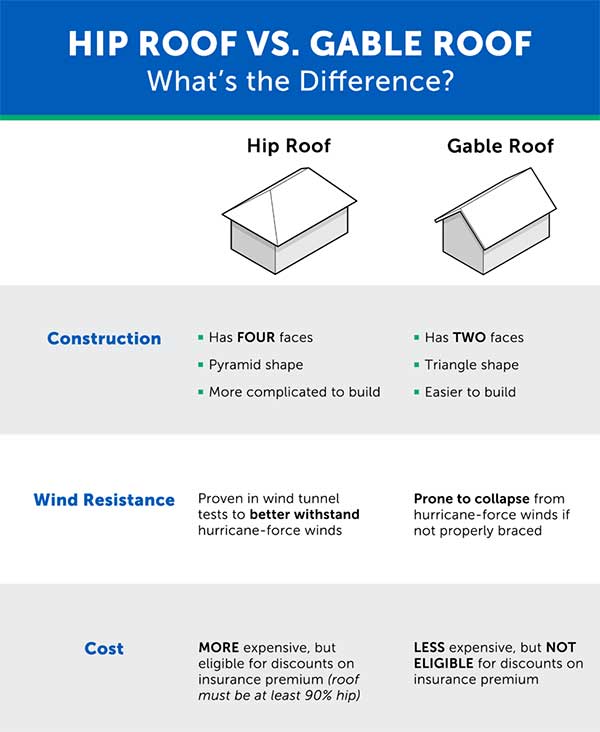

Hip Roof vs. Gable Roof: What’s the Difference?

The roof is your home’s first line of defense against wind, hail, wildfire, and other hazards, and it is considered the most important part of a house to home insurers. Once a home’s roof is breached, it increases the risk of more serious damage claims. This is why the shape of a home’s roof plays an important role in determining homeowner’s insurance rates in Florida.

Let’s take a look at the most common types of roof shapes – hip and gable

Where Is the Home Located?

Where is the Home Located?

Location significantly impacts homeowner’s insurance rates. Florida’s relatively expensive homeowner’s insurance rates can be attributed to the moderate to high risk of hurricanes, floods, and sinkholes throughout the state, and coastal homes may pay higher premiums to compensate for the elevated risk. Consider distance to the shore as you factor in possible insurance costs.

On the contrary,if your home is located within five miles of a fire station or 1,000 feet of a fire hydrant, your home insurance premium may be lower. Take a moment to determine the distance between your house and these features and provide them to your insurance agent.

What Features Are Included?

Certain features of your home can increase your insurance rates, while others are eligible for discounts.*

Features That May Increase Insurance Rates

Inground swimming pool

Hot tub

Custom decorative features

Extensive landscaping

Fireplace or wood-burning stove

Deck

Features That May Decrease Insurance Rates

Features That May Decrease Insurance Rates

Alarm system (burglar and/or fire)

Gated entrance

Wind mitigation

*Not all homeowners insurance companies offer the same discounts or use the same criteria to evaluate whether or not a home is eligible for discounts.

Whether you own or rent a home, apartment or condo in Florida, you will want to protect your investment by selecting the Best Florida Homeowners Insurance Companies in the Florida market, and which you can trust.

Get Your Florida Insurance Quote Now

[gs_logo speed="20000" ticker="1" inf_loop="0"]

Florida Homeowners Insurance Companies

Known for it pristine beaches, parks and holiday resorts, Florida is a wonderful place to call home. There is a lot to love about the lifestyle in the Sunshine state, which of course doesn't necessarily include the money home owners (or renters) pay for their home insurance policies. Of course, the best Florida Homeowners Insurance Companies do compete against each other to offer premiums that are competitive and affordable but as a whole, Florida annual premiums for homeowners insurance are indeed on the higher side.

How much can I expect to pay for my Home Insurance?

Compared to the national average of $1,173 per year, Florida home owners pay an average of just under $2000 per hear for their homeowners insurance premiums. That's quite an increase, and of course, the cost of premium depends on several factors, including where you live, how old your home is, it's value etc...

Why are homeowners insurance premiums more expensive in Florida?

The answer to that question is simple and understandable. Out of the ten most devastating hurricanes in the US, a whooping 7 of them made landfall in Florida, six of them occurring in the years 2004 and 2005.

Notwithstanding the cost of damages in human terms, hurricane often leave behind a trail of devastation that can amount into the billion of dollars. As a whole, the sunshine state is still reeling from the effects of the Irma, a category 4 hurricane that hit the state in 2017.

In addition to Hurricanes, Florida also has to deal with a range of other disasters such as wildfires and tornadoes.

(The information below is valid at the time of writing. It is important to understand that only an insurance agent, who specializes in the Florida marketplace can provide an up-to- date assessment as to which companies offer the best or more affordable deals.)

Tower Hill Group

The second largest insurance provider in Florida, Tower Hill Group provides an extensive range of insurance related services as well as providing options for:

Water damage coverage

Sewer insurance plans

Personal valuables

Protection against identity theft

One of Tower Hill Group premium offer is its Imperial Shield program aimed at high end homes. Unlike other providers, Tower Hill Group offers its own flood insurance, even though in Florida, National Flood Insurance Program is provided by the federal government. For example, Tower Hill's flood insurance can provide home owners coverage for up to $5 million in building replacement costs and a more than generous $2.5 million in home content.

As far as premiums are concerned, Tower Hill certainly makes an effort to be as affordable as the market will allow it to be. It's rates are certainly competitive when compared to other providers.

Ratings: Tower Hill received a A- rating from A.M. Best. A very honorable commendation which means that the company has the financial backbones and the excellence of service to be able to meet its obligations when disaster strikes. (i.e. pay your claims)

State Farm

One of the largest insurance providers in the nation, State Farm is a national insurance known throughout the USA by name and reputation.

Insurance services provided:

Umbrella liability coverage

Personal property coverage

Identity theft coverage

If you are looking for discounts and are willing to combine insurance types into one, then State Farm is an excellent option to consider. A common multi-line discount package would combine both auto and home insurance policies.

Ratings: State Farm has a A++ rating from A.M. Best. (The highest possible ranking)

Citizens Property Insurance Corp.

Also known as the "insurer of last resort", Citizens Property Insurance Corp often time serves as the insurance company of choice for those who's quest for coverage with other providers have proven to be unsuccessful. Be that as it may, let not this accolade deter you for exploring the many options Citizen Property offers. Citizens Property Insurance Corporations is a state backed insurance provider.

With few choices, compared to other providers, Citizens does acquit itself more than honorably when it comes to personal property coverage and sinkhole damage coverage.

[su_highlight background="#ffff99"]Save even more on your homeowners insurance? Consider installing a Fire or Burglar alarm in your home.[/su_highlight]

Ratings: Citizens Property Insurance Corp has a B++ rating from A.M. Best. (Good - B++ is an updated ranking compared to a previous rating of B+)

Other Homeowners Insurance Companies

[su_table]

America Family

Amica

Farmers

Hartford

Liberty Mutual

Metlife

Nationwide

Travelers

USAA

[/su_table]

The Best Florida Homeowners Insurance Companies are a subjective method of grading the companies when comparing they against each other. These ratings are dependent on several factors including customer satisfaction, reader score feedback and satisfaction. When dealing with a Florida based Insurance Agency such as ourselves, we have certainly have access to the most updated data with regards to the the Best Florida Homeowners Insurance Companies.

It is important that you get the right Florida Homeowners Insurance coverage for yourself. Want to save yourself a little money? Make sure you check our article: Spring Maintenance Tips to Protect Your home, which gives you some clues on things you can do right now to your home, apartment or condo that have the potential to reduce your home insurance premiums. If you wonder what the difference is between a condo and a homeowners insurance, you can find some answers here.

We, at LNC Insurance Providers are a family owned insurance agency, in business for over a decade. Our main office is in Miami, but we provide insurance cover throughout the state of Florida. As such we have a unique knowledge and experience of the challenges and realities of all aspects pertaining to Florida Insurance.

Click here for a list of Florida top property & casualty insurance companies

There are many factors to take into consideration when thinking about purchasing a Florida Homeowner Insurance Policy. Here is one consideration that rarely goes into people’s minds when they are about to take the necessary steps to protect their homes: their pets.

It’s a common mistake, after all how could your furry (or not-so-furry) friend affect your homeowners coverage? Yet insurance providers take this issue seriously and consider that your pet, however cute is well capable of causing damage to your property. It is an issue considered to be important enough that in some cases, an animal member of your household may be lead to an insurance denial altogether.

Question: Do you want to know how to choose the best Florida Homeowners Insurance? The answers to that question are provided in our article aptly called: How Do I Choose The Best Homeowners Insurance?

Dogs are among the most common pets in the state of Florida. For all their admirable qualities, dogs are in fact the riskiest pets, if only because they can bite. In fact, according to the Centers for Disease Control and Prevention, in the continental United States of America, 4.5 million people suffer from dog bites each year, with about 900,000 requiring medical treatment. It falls to reason therefore to understand why insurance providers take such a measured approach to this issue.

But before you start pulling your hair in despair, there is a silver lining in all of this: most homeowners insurance policies cover dog bites and other incidents where dogs re involved, even if that means that your homeowners insurance policy might cost you more.

Dogs Companies Will Not Insure

Believe it not, certain breeds have made it to insurance providers list of “bad breeds” and if you happen to own a dog from that list, you might very well have a challenge on your hands. The rule of thumbs on determining what breed is dangerous enough (in the eyes of the insurance providers) to be listed as a member of the “bad breeds”, consider this:

If a dog can inflict serious damage from a single bite, then its breed may find itself on this list. Here is another consideration: the size of the dog is not always a determinant factor either.

A study from the Applied Animal Behavior Science journal says that large dogs, often pigeonholed as the dangerous breeds, aren't any more likely to bite than small ones. Siberian Huskies and Greyhounds, to name a couple, scored as very calm dogs, and even pit bulls and Rottweilers registered average or below-average aggression. The tiny Dachshund, meanwhile, ranked as the journal's most-aggressive breed, with Chihuahuas coming in second. (ref: esurance.com)

Be that as it may, here is a list of dogs that commonly referred to as “bad breeds” by insurance companies:

Akita

Alaskan Malamute

Chow Chow

Doberman

German Shepherd

Pit Bull

Rottweiler

Siberian Husky

Wolf Hybrid

Notwithstanding the above, we encourage you to call your Florida Homeowners Insurance agent for any further clarification.

While most people choose a cat, dog, hamster or bird as their pet, some folks prefer more exotic animals. For example, over 10,000 big cats, and 3,000 apes, are privately owned in the US. These are not your ordinary tamed, domesticated animal and however mild mannered these are, they are still wild in nature and as a result wholly unpredictable.

As such, it is extremely unlikely that any insurance company will cover them under their homeowners insurance policies. If a mountain lion happens to roam inside an enclosure in your backyard, your only option would be to look into exotic pet insurance as they are the only ones that will offer the sky high coverage capable of handling these wild creatures.

Did you know?

There are more captive tigers in the US than there are wild tigers on earth?

Make Sure You Disclose Any Animal Your Own To Your Insurer

Owning an animal is a big responsibility and requires special care and attention. Dogs, as a general rule, can impact any homeowners insurance coverage you seek and it is crucial that you don't hide the fact that you do own a dog, or any other animal from your insurer.

Training your dog is one excellent way to ensure that you are taking your role as a responsible dog parent seriously. In fact, training is so important that some insurers might even give you a break, particularly if your dog gets a "Canine Good Citizen" certificate, obtainable from the AKC.

Whether you own a pet or not, it is important that you get the right Florida Homeowners Insurance coverage for yourself. Want to save yourself a little money? Make sure you check our article: Spring Maintenance Tips to Protect Your home, which gives you some clues on things you can do right now to your home that have the potential to reduce your home insurance premiums. If you wonder what the difference is between a condo and a homeowners insurance, you can find some answers here.

We, at LNC Insurance Providers are a family owned insurance agency, in business for over a decade. Our main office is in Miami, but we provide insurance cover throughout the state of Florida. As such we have a unique knowledge and experience of the challenges and realities of all aspects pertaining to Florida Insurance.

Homeowners insurance in Florida comes under the umbrella of Florida Property Insurance which makes the whole topic a lot more confusing than it should really be. Of course, the ultimate source of information regarding any insurance topic can only be your local insurance agency and for countless Florida residents, that can only mean LNC Insurance Providers.

Being knowledgeable on the issue of Florida Property Insurance in advance of your calling one of our insurance brokers can of course better assist you in ensuring that you get the best possible coverage at the lowest price. And that is precisely what we aim to provide you. The very best Florida Homeowners Insurance.

It’s a reasonable assumption that the more expensive a home might be, the move it will cost to repair/rebuild it when tragedy strikes. And thus, Florida Homeowners Insurance costs are largely driven by the type of home you live in. In Florida, homeowners typically live in any the following five types of residences:

Being knowledgeable on the issue of Florida Property Insurance in advance of your calling one of our insurance brokers can of course better assist you in ensuring that you get the best possible coverage at the lowest price. And that is precisely what we aim to provide you. The very best Florida Homeowners Insurance.

Condos

Townhomes

Traditional Homes

Rental Properties

Manufactured Homes

Insuring either of the above falls under specific criteria and this is one of the topic of conversation you will have with one of our agents.

Where Do You Live

You’ve heard of the old say: “location, location, location”. And in the case of homeowners’ insurance, this piece of street wisdom has never been more accurate. Florida property insurance coverage, including homeowners’ insurance largely depends on where you live. Living by the ocean has its advantages and if you are lucky enough to live there, then you already know that the Florida coastline is always the landing area for any hurricane that might come our way.

How old is your home

Another logical truth about the cost of homeowners insurance is of course the age of the property you live in. This is particularly true in terms of new building codes that were introduced in the aftermath of hurricane Andrews. The age of the property is one of the factors insurance providers take into consideration.

When was the last time you made a claim?

Much like Florida Car Insurances, repeated claims will greatly impact the cost of insuring your home. As much as we all hate to admit it, insurance providers do take a calculated risk anytime they underwrite a policy, and repeated claims might place your insurance policy on a more expensive bracket.

How is your home built?

Another logical assumption: the type of material used in the building of your home greatly influences property insurance rates in Florida. For example, a fire, damaging as it can be can have a more pronounced effect on wooden homes than on brick houses. The take away from this is that a house build with bricks might significantly lower the property insurance costs.

LNC INSURANCE PROVIDERS Offers Tips to Help You Save on Homeowners Insurance

The following tips are the top 10 ways to save money on your Florida Homeowners Insurance.

FLORIDA - Purchasing the Florida Homeowners Insurance that is right for you and your home can be confusing, especially for first-time buyers. By learning the basics on how to get the most for your money, you can save on your homeowners insurance and feel confident you have adequate coverage. LNC INSURANCE PROVIERS a leading insurance agency of homeowners and auto insurance in Florida offers these tips to lead you in the right direction when you purchase your homeowners insurance.

Shop around. In addition to considering friends, family, the phone book or the Internet as possible sources to find homeowners insurance, consult with an independent insurance agent. Look for a wide range of prices from several companies. Remember, you get what you pay for, so look for not only a fair price but excellent service as well. Check a company’s financial rating with A.M. Best or Standard & Poor’s.

Raise your deductible. Companies generally have deductibles (what you pay before your insurance policy kicks in) starting at $250. By choosing a higher deductible ($500, $750, $1,000 or higher), you’ll have lower annual premium payments.

Consider how much insuring a new home will be. The age of your home may qualify you for savings because plumbing, heating and electrical systems of newer homes have lower risks than outdated systems. Construction of the home (brick versus wooden frame) can affect your cost as well, depending on your home’s location. Also, if you live near your local fire department, your homeowners rates might be lower than if you are many miles away.

Insure your home, not your land. Since homeowners policies don’t provide protection for your land, it would be a waste of money to include its value as part of your dwelling coverage, which should only reflect the price it would cost to repair or replace your home’s structure.

Insure your car and home with the same company. You can save money if you have more than one type of policy with the same insurance company. The more good business you give the company, the more valuable you are as a customer.

Improve home security and safety. If your home has certain types of fire alarms, burglar alarms, locks, or smoke detectors, you’ve reduced your risk and may qualify for a credit.

Look for senior discounts. If you are at least 55 years old and retired, your insurance company may offer you a discount. Retirees often spend more time at home and are more likely to spot trouble and prevent a loss.

Look for group coverage. Many insurance companies offer discounts to groups such as alumni or business associations. Check with your association director or employer to see if they offer a plan.

Stay with one insurer. If you keep your coverage under one insurer for several years, you may be offered a discount from the company. The longer you are a customer, the more money you will likely end up saving.

Compare the limits in your policy to the value of your possessions at least once a year. If you make any major purchases or additions, you want to ensure they will be covered, but you do not want to spend more than is necessary.

We are one of Florida's leading Family Owner and Operated Insurance Agencies - Established in 2006

LNC INSURANCE PROVIDERS is an independent insurance agency offering a full range of insurance products including AUTO, HOME, COMMERCIAL, BOAT, MOTORCYCLE, ETC.

We are a five star rated insurance agency on Google!

It’s a reasonable assumption that the more expensive a home might be, the move it will cost to repair/rebuild it when tragedy strikes. And thus, Florida Homeowners Insurance costs are largely driven by the type of home you live in. In Florida, homeowners typically live in any the following five types of residences:

It’s a reasonable assumption that the more expensive a home might be, the move it will cost to repair/rebuild it when tragedy strikes. And thus, Florida Homeowners Insurance costs are largely driven by the type of home you live in. In Florida, homeowners typically live in any the following five types of residences:

LNC INSURANCE PROVIDERS is an independent insurance agency offering a full range of insurance products including AUTO, HOME, COMMERCIAL, BOAT, MOTORCYCLE, ETC.

LNC INSURANCE PROVIDERS is an independent insurance agency offering a full range of insurance products including AUTO, HOME, COMMERCIAL, BOAT, MOTORCYCLE, ETC.