We, at LNC Insurance Provides have been servicing Florida for more than a decade now, and as such, we are fully aware that car insurance rates can vary from company to company. Sometimes these differences can be quite substantial and even within the same city, there can be wide difference in premium costs. Who has cheap car insurance Florida is not as easy as it sounds as we are all too painfully aware of the pitfalls of "cheap" anything entails. The same is true for insurance

It is not uncommon to find cases where car insurance rates say Jacksonville, FL for example to be double, triple and even sometimes quadruple what drivers would pay in different cities. If there is one thing to take away from our analysis, it is that it pays to shop around. Just like you would do if If you were looking for the best rates in any other industry.

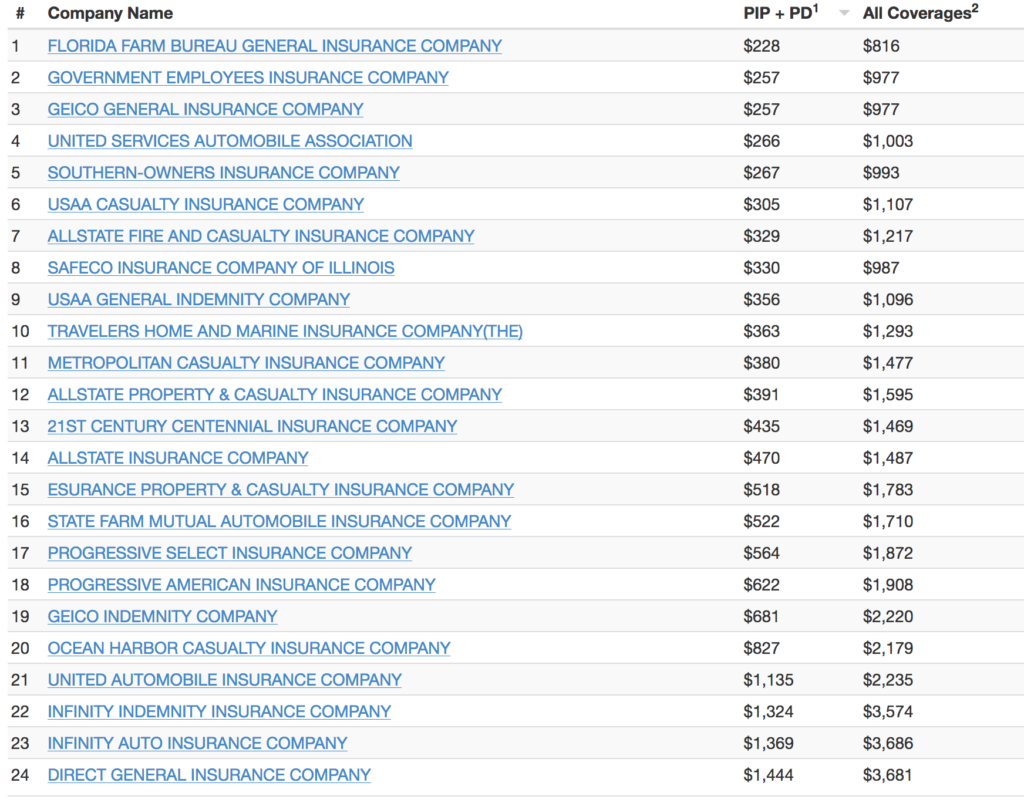

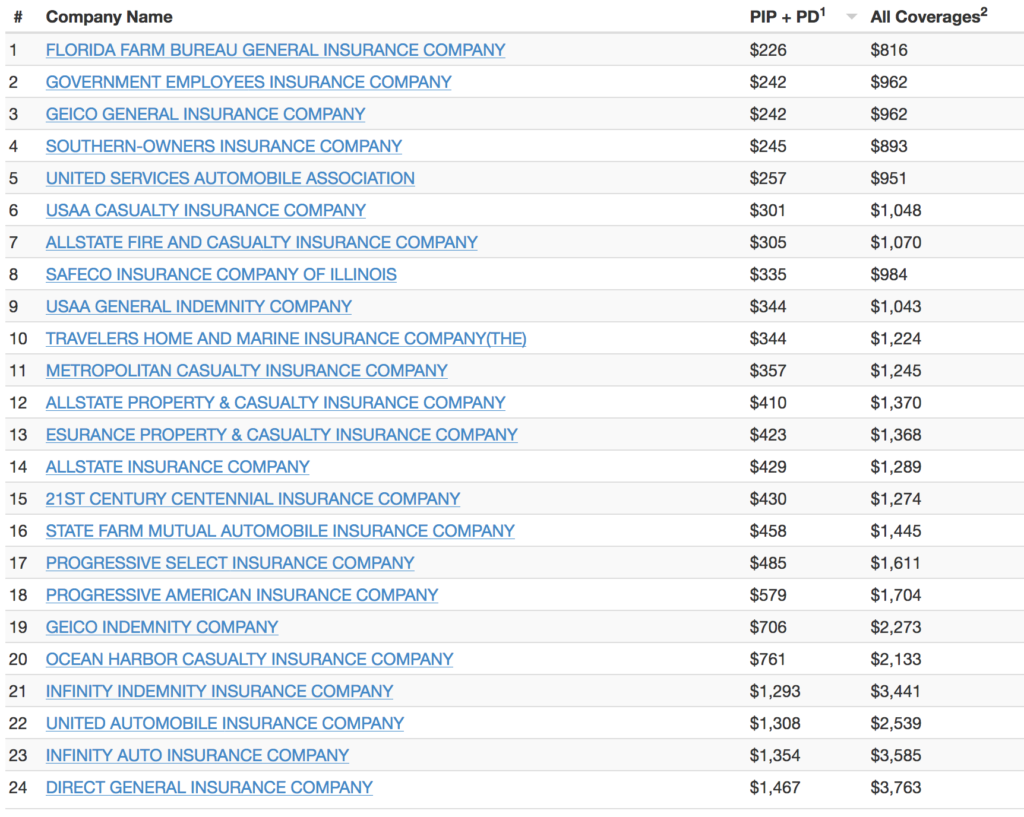

We have included below a table analysis of typical premium costs for companies who offer auto insurance in our great state. It is summary of a Cheap Car Insurance Rates in Florida analysis which will serve as giving you enough information to get ahead.

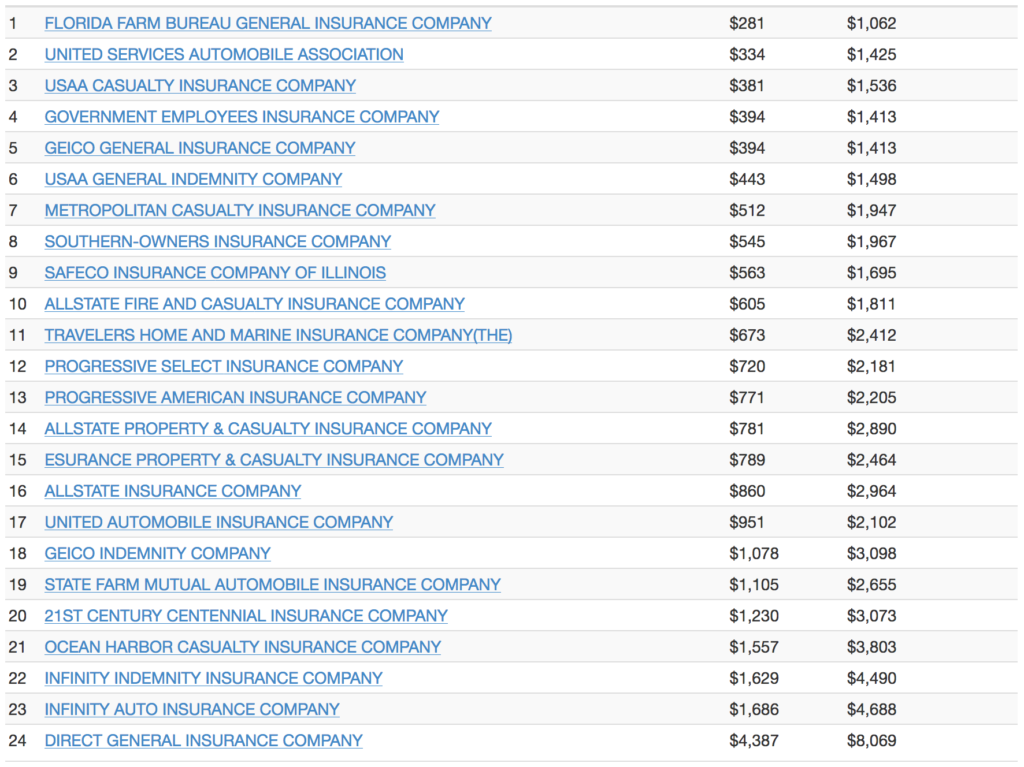

Miami-Dade, FL

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

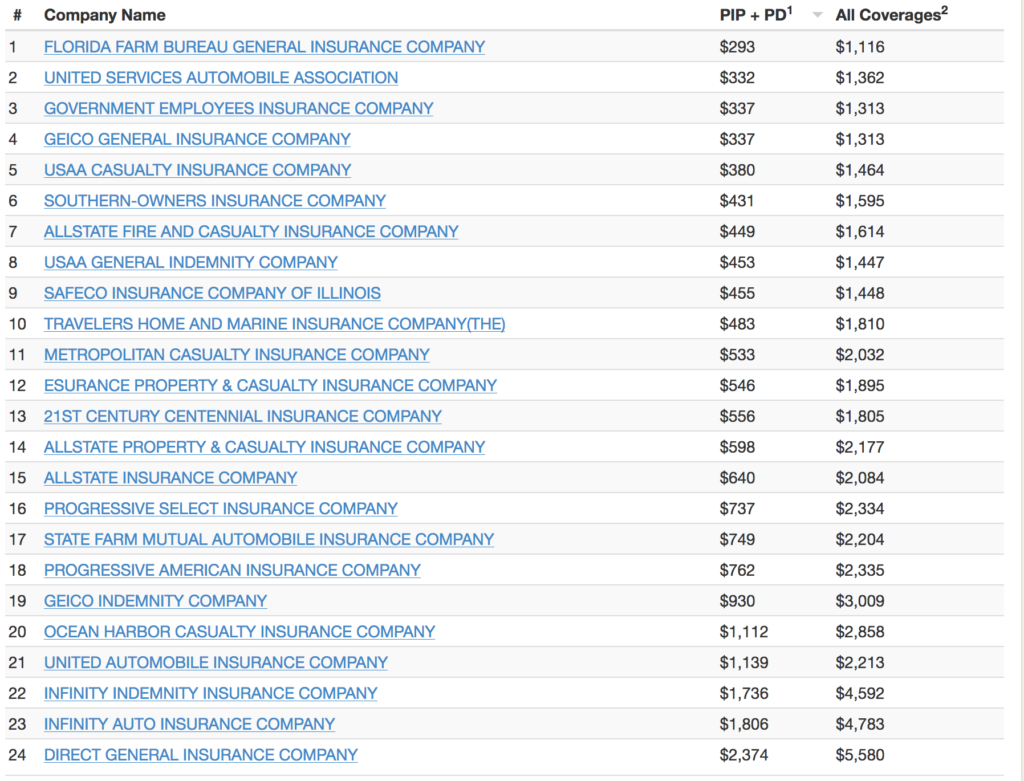

Broward, FL

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

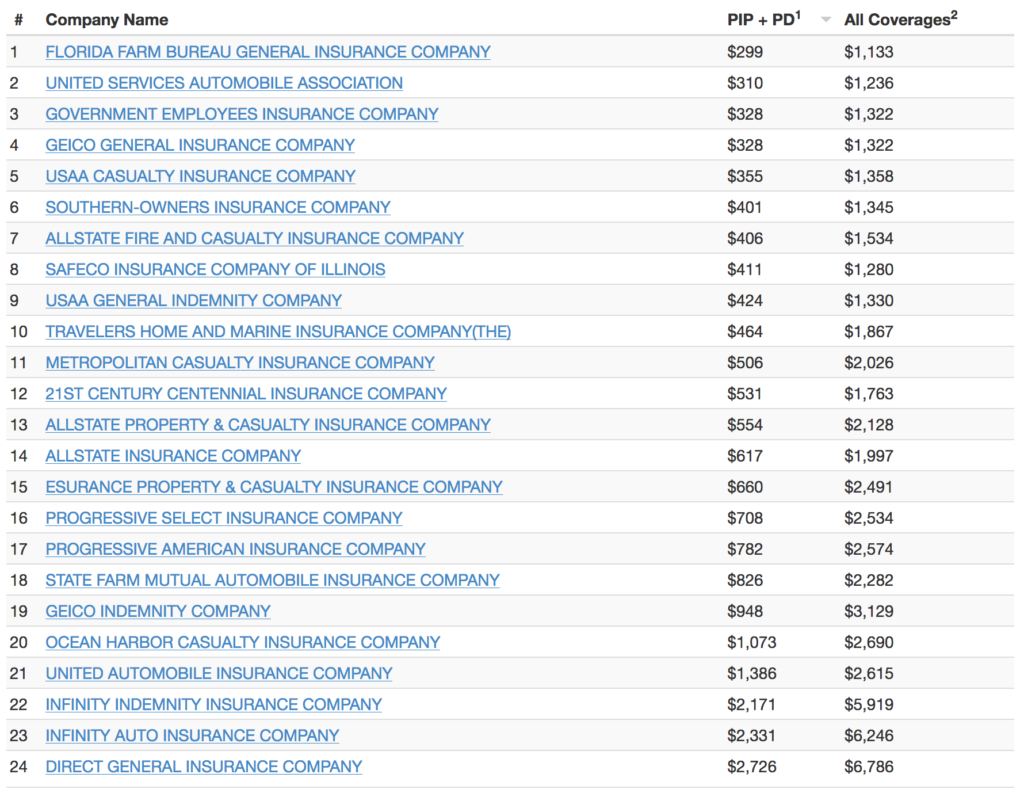

Palm Beach County, FL

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

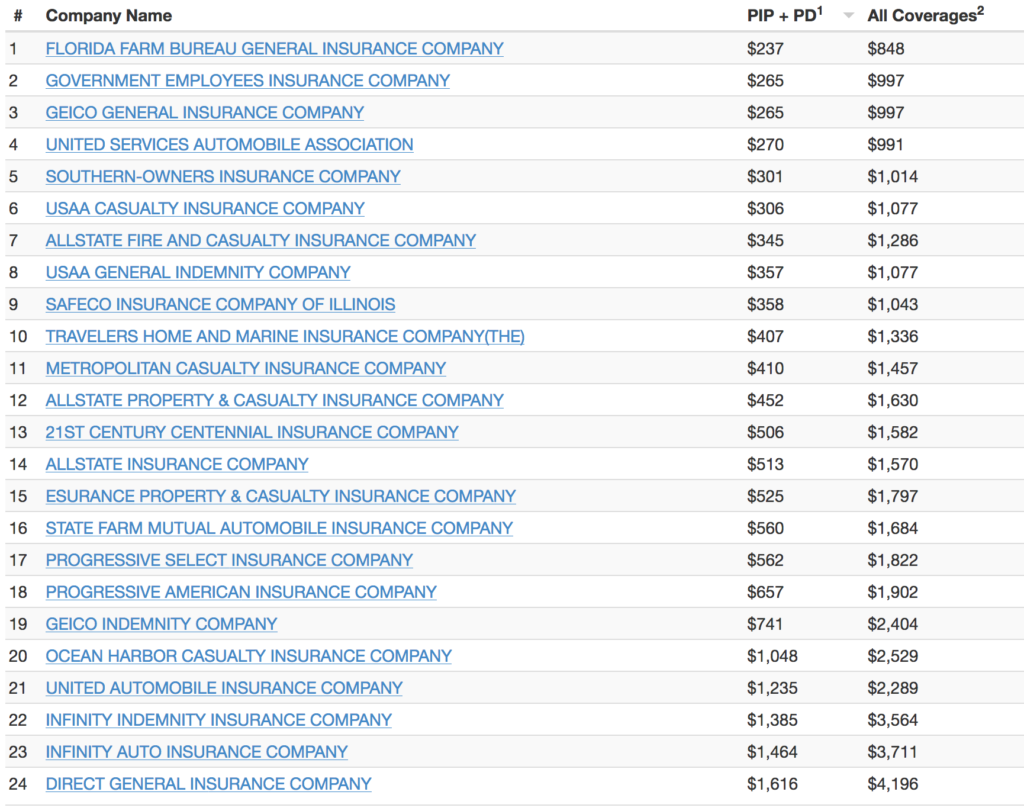

Orange County, FL

Main City: Orlando

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

Pinellas County, FL

Main City: Tampa

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

Duval County, FL

Main City: Jacksonville

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

Lee County, FL

Main Cities: Fort Myers, Cape Coral

Married Male (Age 70), Married Female (Age 65) – One car, no accidents or violations in the last 3 years, pleasure driving use – 6,000 miles per year.

LNC INSURANCE PROVIDERS is an independent insurance agency offering a full range of insurance products including AUTO, HOME, COMMERCIAL, BOAT, MOTORCYCLE, ETC.We are a five star rated insurance agency on Google!

LNC INSURANCE PROVIDERS is an independent insurance agency offering a full range of insurance products including AUTO, HOME, COMMERCIAL, BOAT, MOTORCYCLE, ETC.We are a five star rated insurance agency on Google!

“The marine industry has delivered hybrid powered vessels that use the latest, state-of-the-art technology while reducing fuel consumption,” said LIZ FERNANDEZ, President for LNC INSURANCE PROVIDERS.LNC INSURANCE PROVIDERS, closely follow the newest developments in boating to meet our customers needs with the best marine insurance products and services.

“The marine industry has delivered hybrid powered vessels that use the latest, state-of-the-art technology while reducing fuel consumption,” said LIZ FERNANDEZ, President for LNC INSURANCE PROVIDERS.LNC INSURANCE PROVIDERS, closely follow the newest developments in boating to meet our customers needs with the best marine insurance products and services.

Over the past few years, businesses have come under increasing pressure to trim their running expenses in order to stay afloat. Companies can look for savings in a variety of ways and unfortunately, sometimes may decide to take a gamble on the inherent foundation of their business investment: Florida BOP Insurance

Over the past few years, businesses have come under increasing pressure to trim their running expenses in order to stay afloat. Companies can look for savings in a variety of ways and unfortunately, sometimes may decide to take a gamble on the inherent foundation of their business investment: Florida BOP Insurance

Differences:

Differences: