How much does restaurant insurance cost in Florida?

The cost of restaurant insurance depends on the policies you choose, the unique risks your restaurant faces, and the value of your business property. Cost estimates are sourced from policies purchased by L and C Insurance customers.

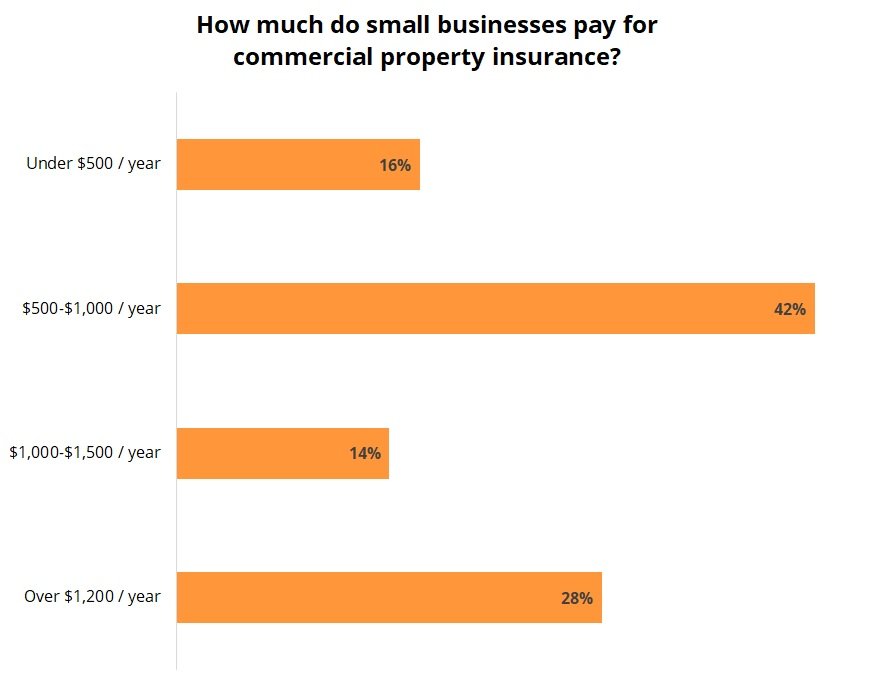

Business owner’s policy costs for restaurants

Restaurant owners typically pay about $175 per month for a business owner’s policy (BOP), or a median annual premium of $2,080. The median value eliminates high and low outliers, providing better representation of typical restaurant insurance costs than the average value.

A BOP bundles general liability insurance with property insurance, usually at a discounted rate. Pricing is determined by your restaurant’s location, operations, and value of business property and equipment.

This policy may include business interruption insurance, which covers income lost at your restaurant due to an unexpected closure.

Median cost per year: $2,030

Policy limit: $1 million per occurrence

Policy deductible: $1,000

Learn how to save money on your policy, which coverage limits to choose. Call L and C Insurance Providers at 888-913-6988

Workers’ compensation costs for restaurants

The median cost of workers’ compensation insurance is about $125 per month for a restaurant, or $1,480 annually. The cost of a policy varies significantly depending on the state and your business operations.

Workers’ compensation insurance is required in almost every state for businesses with employees. Even when it’s not required, it’s a smart purchase in the restaurant industry, where employees routinely cut, chop, and fry in hot oil.

This coverage helps pay medical costs and lost wages for employees who are injured on the job. Most policies include employer’s liability insurance, which protects restaurant owners against lawsuits related to workplace injuries.

Compare restaurant insurance quotes from top U.S. carriers

Get Quotes

Liquor liability insurance costs for restaurants

The median cost of liquor liability insurance is about $45 per month for a restaurant, or $545 annually. This policy protects restaurants that serve alcohol from liability for the actions of intoxicated customers. In some jurisdictions, your restaurant might need liquor liability insurance in order to obtain a liquor license.

Median cost per year: $545

Generic policy limit: $1 million

General liability costs for restaurants

Restaurants pay a median premium of less than $70 per month for general liability insurance, or $805 annually. This policy protects restaurants against customer injuries and customer property damage, along with advertising injuries.

Insureon’s licensed agents typically recommend purchasing a business owner’s policy, which bundles general liability insurance with commercial property insurance at a discounted rate. It protects your own business property along with covering common business risks.

Median cost per year: $805

Policy limit: $1 million per occurrence

Policy deductible: None